India’s Non-Banking Financial Company (NBFC) sector is growing rapidly with the rise of digital lending, fintech innovation, embedded finance, and AI-driven credit decisioning. As competition increases and RBI compliance requirements become stricter, NBFCs need a powerful, scalable, and intelligent Loan Management System (LMS) that can automate operations, reduce risks, and improve customer experience.

This is where Roopya stands out as one of the most advanced and trusted Loan Management Systems for NBFCs in India.

Roopya is an AI-first, cloud-native, no-code lending platform designed specifically for NBFCs, microfinance institutions, fintech companies, banks, and digital lenders. The platform helps lenders manage the complete lending lifecycle — from loan origination and underwriting to disbursement, collections, analytics, and compliance.

What is a Loan Management System (LMS)?

A Loan Management System is software that automates and manages every stage of the loan lifecycle. It enables NBFCs to process loan applications, evaluate borrower eligibility, disburse funds, track repayments, manage collections, generate reports, and ensure compliance with RBI regulations.

Modern LMS platforms are no longer limited to simple repayment tracking. Today’s NBFCs require intelligent systems with:

- AI-powered underwriting

- Automated collections

- Digital KYC

- Credit bureau integrations

- Payment gateway support

- Customer portals

- Analytics dashboards

- Regulatory reporting

- API-based integrations

Roopya provides all these capabilities through a unified digital lending ecosystem.

Why NBFCs in India Need Advanced Loan Management Software

Traditional lending processes are slow, manual, and prone to operational inefficiencies. Many NBFCs still rely on spreadsheets, fragmented systems, and manual approvals, which lead to:

- Delayed loan approvals

- Higher operational costs

- Compliance risks

- Poor borrower experience

- Increased NPAs

- Limited scalability

- Manual reconciliation issues

According to discussions among Indian fintech professionals and NBFC operators, lenders now prioritize features like co-lending support, no-code workflows, daily EMI calculations, automated reconciliation, and RBI-compliant servicing.

Roopya solves these challenges through automation, AI, analytics, and cloud infrastructure.

Key Reasons Why Roopya is the Best LMS for NBFCs in India

1. Complete End-to-End Lending Automation

Roopya automates the complete loan journey including:

- Loan applications

- KYC verification

- Credit assessment

- Loan underwriting

- Approval workflows

- Disbursement

- EMI tracking

- Collections

- Recovery management

- Reporting

This eliminates manual dependency and significantly reduces processing time.

The platform enables NBFCs to process loans faster while maintaining accuracy and compliance.

2. AI-Powered Credit Decisioning

One of Roopya’s biggest strengths is its AI-first approach.

The platform uses machine learning and advanced analytics for:

- Credit scoring

- Fraud detection

- Risk profiling

- Predictive underwriting

- Delinquency prediction

- Portfolio analysis

Roopya integrates with major credit bureaus including:

- CIBIL

- Experian

- Equifax

- CRIF

This allows lenders to make faster and smarter credit decisions while minimizing defaults.

3. No-Code Lending Platform

Roopya is designed as a no-code LMS platform, allowing NBFCs to configure:

- Loan products

- Interest structures

- Approval workflows

- Repayment schedules

- Collection rules

- User permissions

- Business policies

without requiring technical expertise or development teams.

This gives business teams complete flexibility and faster go-to-market capability.

4. Cloud-Native Infrastructure

Roopya is built on modern cloud architecture that offers:

- High scalability

- 99.9% uptime

- Faster performance

- Enterprise-grade security

- Automatic updates

- Remote accessibility

- Disaster recovery

Cloud-native infrastructure is essential for fast-growing NBFCs handling large loan portfolios and multi-branch operations.

5. RBI Compliance & Regulatory Reporting

Compliance is one of the most critical aspects for Indian NBFCs.

Roopya helps NBFCs comply with:

- RBI guidelines

- KYC norms

- AML regulations

- Fair Practices Code

- GST reporting

- TDS reporting

- Audit trail requirements

- Credit bureau reporting

The platform also supports regulatory dashboards and automated compliance reporting, reducing operational risk.

6. Faster Loan Processing

Modern borrowers expect instant approvals and digital onboarding.

Roopya enables:

- Digital applications

- Real-time eligibility checks

- e-KYC verification

- Digital signatures

- Automated approvals

- Instant disbursement workflows

This dramatically reduces turnaround time and improves customer satisfaction.

7. Advanced Collection & Recovery Management

Collections are critical for NBFC profitability.

Roopya provides intelligent collection features including:

- Automated reminders

- WhatsApp notifications

- SMS alerts

- Email reminders

- DPD tracking

- Agent assignment

- Promise-to-pay tracking

- Settlement workflows

- Legal case management

AI-driven collections help reduce delinquency and improve recovery efficiency.

8. Multi-Channel Payment Integration

Roopya integrates with leading payment gateways and banking systems including:

- Razorpay

- PayU

- CCAvenue

- NACH/eNACH

- UPI systems

- Banking APIs

The platform supports:

- EMI automation

- Auto-debit

- Payment reconciliation

- Refund handling

- Real-time payment tracking

This improves repayment efficiency and reduces manual accounting effort.

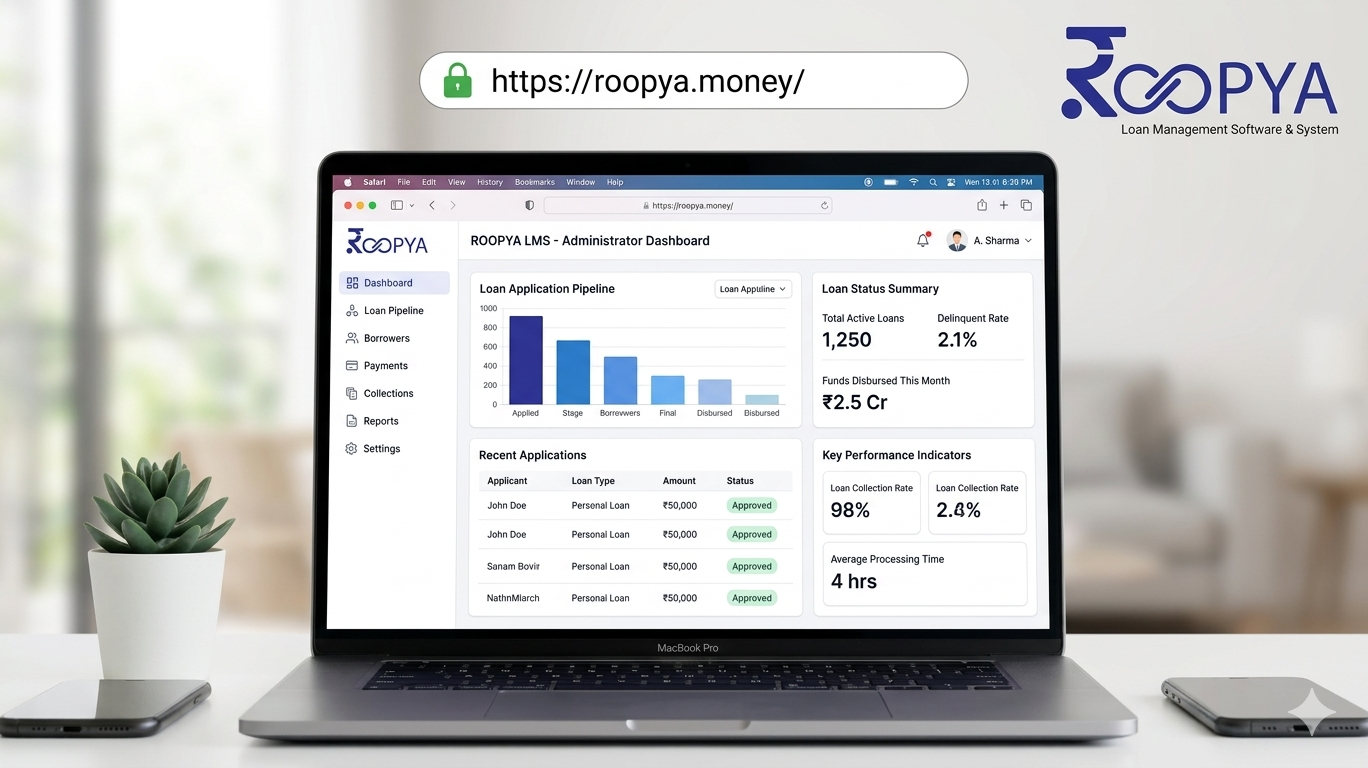

9. Powerful Analytics & Business Intelligence

Roopya provides advanced analytics dashboards for:

- Portfolio performance

- Loan disbursement trends

- Approval rates

- Rejection analysis

- Collection efficiency

- Risk exposure

- Vintage analysis

- Cohort tracking

These insights help NBFCs make data-driven business decisions and improve profitability.

10. Seamless Integrations

Roopya supports API-based integrations with:

- Credit bureaus

- Banks

- Payment gateways

- Accounting software

- CRM systems

- SMS gateways

- WhatsApp APIs

- KYC providers

The platform’s open API infrastructure enables easy scalability and ecosystem connectivity.

11. Superior Customer Experience

Customer experience is now a competitive differentiator for lenders.

Roopya offers:

- Self-service borrower portals

- EMI payment dashboards

- Digital statements

- Online service requests

- NOC generation

- Mobile-friendly access

Borrowers can manage their loans digitally without visiting branches.

12. Supports Multiple Lending Segments

Roopya is highly flexible and supports:

- Personal loans

- Business loans

- MSME lending

- Gold loans

- Vehicle finance

- Consumer durable loans

- Microfinance

- Education loans

- Co-lending

- Supply chain finance

This makes it ideal for diversified NBFC portfolios.

13. Enhanced Security & Data Protection

Security is essential for financial institutions.

Roopya provides:

- Data encryption

- Role-based access control

- Multi-factor authentication

- Secure cloud hosting

- Audit trails

- Backup systems

- Disaster recovery

The platform is designed with enterprise-grade security standards.

14. Quick Implementation & Faster Go-Live

Traditional LMS implementation can take months.

Roopya offers:

- Rapid onboarding

- Sandbox testing

- Quick configuration

- Dedicated implementation support

- Go-live in days

This helps NBFCs launch faster and reduce implementation costs.

Benefits of Using Roopya LMS for NBFCs

Operational Efficiency

Automation reduces manual tasks and operational costs.

Faster Loan Approval

AI-driven workflows accelerate processing.

Lower Default Risk

Advanced analytics improve credit quality.

Better Compliance

Automated reporting reduces regulatory risk.

Improved Customer Retention

Digital experiences enhance borrower satisfaction.

Scalability

Cloud infrastructure supports business growth.

Higher Recovery Rates

AI-powered collections improve repayment efficiency.

Why Roopya is Better Than Traditional NBFC Software

| Feature | Traditional LMS | Roopya LMS |

|---|---|---|

| Cloud Native | Limited | Yes |

| AI-Powered Underwriting | No | Yes |

| No-Code Configuration | No | Yes |

| Real-Time Analytics | Limited | Advanced |

| Automated Collections | Basic | AI-Based |

| Digital Onboarding | Partial | Complete |

| RBI Compliance Tools | Limited | Comprehensive |

| API Integrations | Limited | Extensive |

| Multi-Channel Lending | Limited | Yes |

| Scalability | Moderate | Enterprise Grade |

Industries Using Roopya Lending Software

Roopya serves:

- NBFCs

- Fintech startups

- Microfinance institutions

- Digital lenders

- Banks

- Co-lending platforms

- P2P lenders

- Embedded finance companies

Future of Digital Lending in India

India’s digital lending market is expanding rapidly with:

- AI-based underwriting

- Embedded lending

- UPI credit systems

- Open banking

- Account Aggregator framework

- Digital KYC

- Automated collections

NBFCs adopting intelligent lending systems will gain a major competitive advantage in the coming years.

Roopya’s AI-first architecture positions it strongly for the future of Indian lending technology.

Roopya has emerged as one of the best Loan Management Systems for NBFCs in India because it combines AI, automation, compliance, scalability, analytics, and customer-centric digital experiences into one powerful platform.

For NBFCs looking to modernize operations, reduce costs, improve collections, enhance compliance, and scale rapidly, Roopya offers a future-ready lending infrastructure built specifically for the Indian financial ecosystem.

Its no-code flexibility, cloud-native architecture, AI-driven decisioning, and comprehensive lending modules make it an ideal solution for modern lenders seeking digital transformation.

Whether you are a startup NBFC, a growing fintech lender, or an enterprise-scale financial institution, Roopya provides the technology foundation required to succeed in India’s evolving lending landscape.

FAQs

1. What is Roopya Loan Management System?

Roopya is an AI-powered, cloud-native Loan Management System designed for NBFCs, fintech companies, and digital lenders to automate the complete loan lifecycle.

2. Is Roopya suitable for NBFCs in India?

Yes, Roopya is specifically designed for Indian NBFCs and supports RBI compliance, KYC, AML, collections, and digital lending operations.

3. Does Roopya support loan origination?

Yes, Roopya includes a complete Loan Origination System (LOS) with digital onboarding, credit scoring, underwriting, and approval workflows.

4. Which credit bureaus does Roopya integrate with?

Roopya integrates with CIBIL, Experian, Equifax, and CRIF.

5. Can Roopya automate collections?

Yes, Roopya offers AI-powered collections, automated reminders, DPD tracking, and recovery management tools.

6. Is Roopya cloud-based?

Yes, Roopya is a cloud-native platform with enterprise-grade scalability and security.

7. Does Roopya provide API integrations?

Yes, Roopya supports APIs for payment gateways, banking systems, bureaus, KYC providers, and third-party services.

8. How quickly can an NBFC implement Roopya?

Roopya offers rapid implementation and onboarding, enabling lenders to go live within days.