Market Overview:

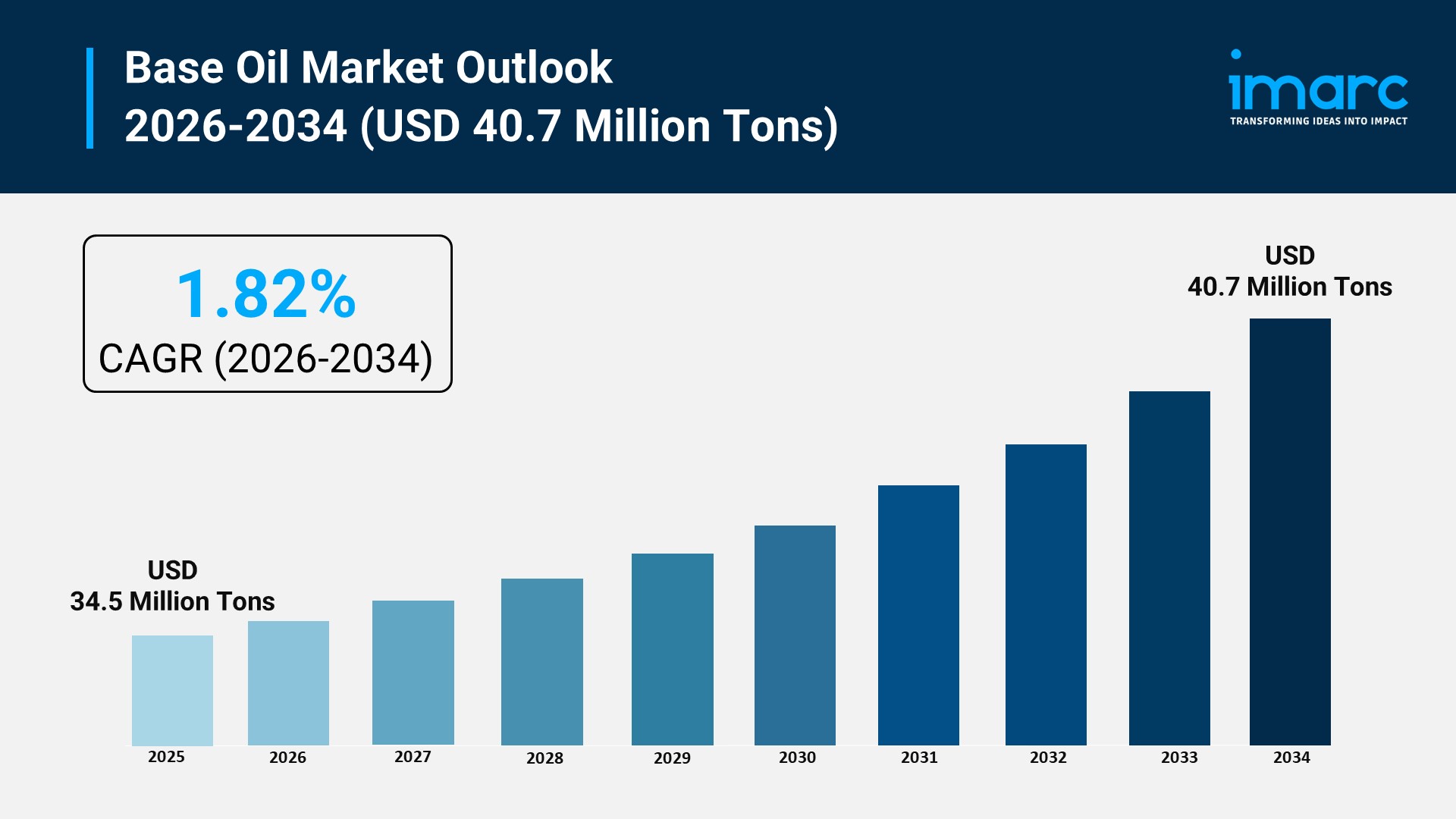

The base oil market is experiencing rapid growth, driven by expanding automotive manufacturing and logistics networks, accelerating industrial automation and heavy machinery deployment, and strict government regulations on emissions and fuel efficiency. According to IMARC Group’s latest research publication, “Base Oil Market Report by Type (Mineral, Synthetic, Bio-Based), Group (Group I, Group II, Group III, Group IV, Group V), Application (Automotive Oil, Industrial Oil, Metalworking Fluids, Hydraulic Oil, Greases, and Others), and Region 2026-2034”, The global base oil market size reached 34.5 Million Tons in 2025. Looking forward, IMARC Group expects the market to reach 40.7 Million Tons by 2034, exhibiting a growth rate (CAGR) of 1.82% during 2026-2034.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

Download a sample PDF of this report: https://www.imarcgroup.com/base-oil-market/requestsample

Our report includes:

- Market Dynamics

- Market Trends and Market Outlook

- Competitive Analysis

- Industry Segmentation

- Strategic Recommendations

Growth Factors in the Base Oil Market

- Expanding Automotive Manufacturing and Logistics Networks

The continuous expansion of global automotive production combined with expanding logistics networks serves as a core driver for the industry. Millions of new passenger cars and commercial vehicles enter international roadways annually, each requiring substantial initial factory fills and scheduled maintenance fluids. High-performance engine formulations rely heavily on premium base oils to satisfy tight mechanical clearances, control engine friction, and extend service intervals under harsh conditions. Major transportation enterprises and fleet operators are scaling their heavy-duty operations across developing logistics corridors, dramatically multiplying the consumption of engine oils, gear lubricants, and transmission fluids. This massive operational expansion requires substantial volumes of reliable lubricating foundations to protect critical driveline components from premature mechanical wear. Consequently, the unrelenting demand for moving goods and people ensures that automotive lubrication remains a massive and steady consuming segment globally.

- Accelerating Industrial Automation and Heavy Machinery Deployment

Rapid industrialization along with the widespread deployment of automated manufacturing infrastructure significantly fuels the consumption of high-grade processing fluids. Modern industrial facilities utilize sophisticated multi-axis robotics, high-capacity hydraulic systems, and complex turbine networks that function continuously under immense thermal and mechanical pressure. These advanced automated systems depend on high-viscosity index formulations to minimize friction, dissipate heat, and prevent costly operational downtime. Industrial machinery manufacturers now dictate strict lubricant performance specifications, forcing plant managers to purchase premium finished lubricants manufactured from highly refined base stocks. Additionally, massive infrastructure construction projects and growing mining operations across developing economic zones heavily utilize heavy machinery that consumes substantial quantities of specialized industrial oils. The steady modernization of factories and heavy machinery operations worldwide guarantees an expanding footprint for specialized industrial lubricating products.

- Strict Government Regulations on Emissions and Fuel Efficiency

Stringent environmental mandates established by international regulatory bodies are fundamentally shifting processing requirements and driving overall market value. Environmental agencies globally are enforcing strict limits on greenhouse gas emissions while demanding higher fuel efficiency standards from automotive manufacturers. To comply with these legal frameworks, original equipment manufacturers are building modern, compact engines that operate at significantly higher temperatures and tighter tolerances. These advanced engines cannot function properly with traditional, low-grade processing fluids due to volatility and oxidation issues. As a result, lubricant blenders are compelled to significantly increase their utilization of highly refined stocks that offer superior thermal stability and lower volatile emissions. This regulatory shift forces a widespread industrial migration toward high-performance formulations, accelerating substantial capital investments in advanced refining infrastructure worldwide.

Key Trends in the Base Oil Market

- Structural Transition Toward Group II and Group III Formulations

The global marketplace is experiencing a major structural shift as blending facilities rapidly replace traditional Group I stocks with advanced Group II and Group III variants. Group I production facilities are closing down globally due to high sulfur content and poor viscosity performance under extreme temperature conditions. Conversely, advanced hydrocracked and hydroisomerized processing oils are witnessing widespread adoption because they provide exceptional oxidation resistance, excellent low-temperature fluidity, and low volatility. Blending operations utilize these highly refined stocks to formulate top-tier synthetic and semi-synthetic lubricants that meet modern engineering guidelines. Original equipment manufacturers increasingly mandate these premium performance profiles for factory-fill applications to ensure component longevity and optimize modern system efficiency. This massive industry-wide transition is transforming refining priorities, turning premium hydroprocessed stocks into the dominant baseline materials for modern lubricant blending plants.

- Development of Tailored Fluid Formulations for Electric Vehicles

The rapid market adoption of electric and hybrid transport options is driving the development of specialized, low-viscosity fluid formulations. Traditional internal combustion engine lubricants focus primarily on mitigating friction within pistons and valvetrains, whereas electric drivetrains present entirely unique fluid dynamics. Electric vehicle fluids require exceptional thermal conductivity to cool rapidly spinning e-motors, alongside excellent dielectric properties to prevent dangerous electrical arcing across high-voltage components. Furthermore, these fluids must offer superior copper corrosion protection because copper is extensively utilized in electric motor windings and internal wiring assemblies. Major refining enterprises and additive manufacturers are co-developing innovative, ultra-low viscosity fluids designed explicitly for integrated electric drive units. This specialized product development represents an entirely new, highly technical market segment that is completely redefining traditional formulation methodologies.

- Rising Utilization of Bio-Based and Re-Refined Eco-Friendly Feedstocks

Growing corporate sustainability targets and circular economy initiatives are driving significant market interest in bio-based and re-refined alternatives. Industrial users and automotive consumers are actively seeking sustainable fluids derived from renewable agricultural sources or advanced used-oil recycling facilities. Modern re-refining plants utilize advanced vacuum distillation and hydrotreating technologies to transform spent lubricants back into high-quality base materials that match the performance of virgin stocks. At the same time, biodegradable bio-lubricants formulated from natural esters are becoming mandatory in environmentally sensitive sectors like marine transport, forestry, and open-pit mining operations. Government procurement policies frequently favor products containing verified recycled or bio-based content, prompting major blenders to diversify their raw material supply chains. This growing ecological focus is successfully transforming used oil from an environmental waste issue into a highly valued sustainable asset.

Leading Companies Operating in the Base Oil Industry:

- Abu Dhabi National Oil Company

- Bharat Petroleum Corporation Limited

- BP plc

- Chevron Corporation

- China National Petroleum Corporation

- China Petroleum & Chemical Corporation

- Evonik Industries AG

- Exxon Mobil Corporation

- Petroliam Nasional Berhad (PETRONAS)

- Phillips 66 Company

- PT Pertamina (Persero)

- Repsol S.A.

- Saudi Arabian Oil Co.

- Shell plc

- TotalEnergies SE

Base Oil Market Report Segmentation:

By Type:

- Mineral

- Synthetic

- Bio-Based

Mineral base oil dominates the market due to its availability and cost-effectiveness, widely used in automotive oils, industrial lubricants, and hydraulic fluids.

By Group:

- Group I

- Group II

- Group III

- Group IV

- Group V

Group I holds the largest market share, favored for its cost-effectiveness and performance in general-purpose lubricants, especially in regions with established refining infrastructure.

By Application:

- Automotive Oil

- Industrial Oil

- Metalworking Fluids

- Hydraulic Oil

- Greases

- Others

Automotive oil leads the segment, driven by rising vehicle ownership and the demand for high-performance oils, particularly in the context of fuel-efficient and low-emission vehicles.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Asia Pacific is the largest regional market for base oil, encompassing major countries like China, Japan, and India.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-201971-6302