The lending industry has undergone a massive digital transformation over the last few years. Banks, NBFCs, fintech companies, and digital lenders are rapidly replacing manual loan processing with intelligent loan origination software that automates every stage of the lending journey.

However, selecting the right Loan Origination Software (LOS) is not as simple as comparing prices or choosing the vendor with the longest feature list. The wrong decision can lead to implementation delays, compliance issues, poor customer experience, and increased operational costs.

Before investing in any lending platform, organizations should evaluate whether the software truly supports their business goals, regulatory requirements, and future scalability.

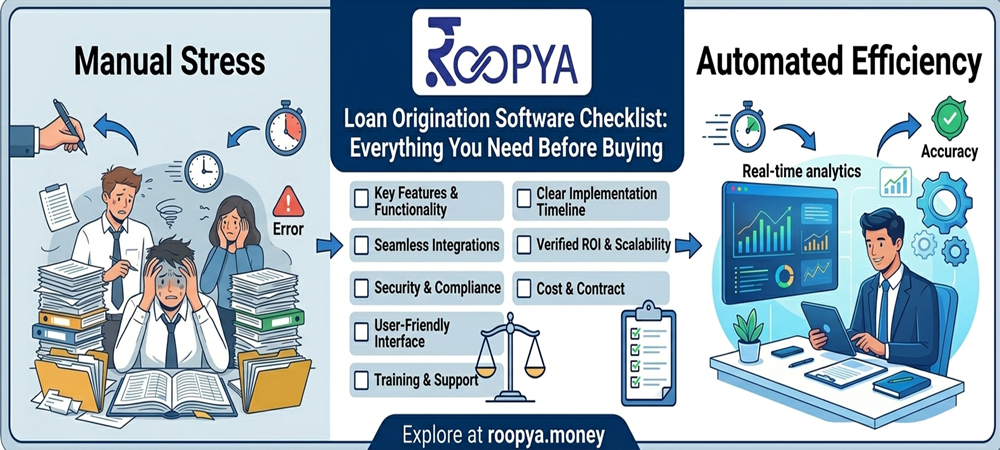

This comprehensive checklist will help lenders make an informed decision before purchasing a Loan Origination Software solution.

What is Loan Origination Software?

Loan Origination Software is a digital platform that manages the complete lifecycle of a loan application—from customer onboarding and document collection to credit assessment, underwriting, approval, and loan disbursement.

Instead of relying on spreadsheets, emails, and paper documents, lenders can automate workflows, reduce processing time, improve compliance, and deliver a better borrower experience.

Modern LOS platforms also integrate AI, OCR, API-based verification, business rule engines, and analytics to enable faster and smarter lending decisions.

Why Choosing the Right LOS Matters

An effective Loan Origination System helps lenders:

- Reduce loan processing time

- Eliminate manual paperwork

- Improve operational efficiency

- Automate underwriting

- Minimize fraud risks

- Ensure regulatory compliance

- Enhance customer experience

- Scale lending operations efficiently

Choosing software without proper evaluation may create bottlenecks that impact profitability and growth.

The Ultimate Loan Origination Software Checklist

1. Digital Customer Onboarding

The first interaction with borrowers should be simple and frictionless.

Check whether the platform offers:

- Online application forms

- Mobile-friendly interface

- Aadhaar and PAN verification

- OTP authentication

- Video KYC support

- eKYC integrations

- Digital signatures

A seamless onboarding experience significantly reduces application abandonment.

2. Automated KYC Verification

Manual KYC consumes valuable operational time.

Your LOS should automate:

- Identity verification

- Address validation

- Document authentication

- PAN validation

- Aadhaar verification

- Face matching

- OCR document extraction

Automated verification improves speed while reducing human errors.

3. Configurable Loan Workflows

Every lender has unique approval processes.

Look for software that allows:

- Custom approval stages

- Product-specific workflows

- Multi-level authorization

- Branch-based routing

- Maker-checker processes

- Conditional approvals

Flexible workflows eliminate dependency on software developers.

4. Business Rule Engine (BRE)

One of the most important features of a modern LOS is a no-code Business Rule Engine.

It should allow lenders to configure:

- Income eligibility

- Credit score cutoffs

- FOIR calculations

- Age limits

- Employment checks

- Geographic restrictions

- Product-specific eligibility

Automated decision-making reduces turnaround time significantly.

5. Credit Bureau Integration

Reliable underwriting depends on credit data.

Ensure the platform supports integrations with:

- CIBIL

- Experian

- Equifax

- CRIF High Mark

Real-time bureau checks improve credit assessment and reduce default risk.

6. AI-Powered Underwriting

Artificial Intelligence is redefining digital lending.

Advanced platforms should provide:

- Automated risk scoring

- Fraud detection

- Predictive analytics

- Alternate data evaluation

- Income estimation

- Behavioral scoring

AI enables lenders to make faster and more accurate credit decisions.

7. Document Management System

Loan files often contain dozens of documents.

An ideal LOS should provide:

- Centralized document storage

- Version control

- OCR extraction

- Auto-tagging

- Secure access controls

- Instant retrieval

Proper document management reduces administrative burden.

8. API Integration Capabilities

Your software should connect seamlessly with external systems.

Check support for:

- Banking APIs

- Payment gateways

- eSign providers

- KYC vendors

- CRM systems

- Accounting software

- Collection platforms

Open APIs make future expansion much easier.

9. Multi-Product Lending Support

Many lenders offer more than one financial product.

The LOS should support:

- Personal loans

- Business loans

- MSME loans

- Gold loans

- Vehicle loans

- Education loans

- Consumer finance

- Mortgage lending

Managing multiple products within one platform improves efficiency.

10. Loan Application Tracking

Borrowers expect transparency.

Look for:

- Real-time status updates

- Automated notifications

- SMS alerts

- Email communication

- Customer portals

- Mobile tracking

This improves customer satisfaction while reducing support queries.

11. Compliance & Regulatory Readiness

Financial regulations evolve constantly.

Ensure your LOS supports:

- RBI compliance

- Audit trails

- Consent management

- Data encryption

- Secure storage

- Role-based access

- Activity logs

Compliance should be built into the platform—not added later.

12. Security Features

Sensitive financial information requires enterprise-grade protection.

Verify:

- Cloud security

- Data encryption

- Multi-factor authentication

- Role-based permissions

- Secure backups

- Disaster recovery

- Audit logging

Security failures can damage reputation and attract penalties.

13. Scalability

Your lending business may grow rapidly.

The software should easily handle:

- Higher application volumes

- Multiple branches

- Multiple teams

- New loan products

- Geographic expansion

- API scaling

Cloud-native platforms generally offer better scalability.

14. Analytics and Reporting

Data-driven lending improves profitability.

Look for dashboards covering:

- Approval rates

- TAT reports

- Pipeline monitoring

- Portfolio insights

- Conversion ratios

- Branch performance

- Credit trends

Advanced analytics support better strategic decisions.

15. Mobile Accessibility

Today’s borrowers expect mobile-first experiences.

A quality LOS should support:

- Mobile applications

- Responsive web portals

- Digital uploads

- Mobile approvals

- Field officer access

Mobile capabilities improve customer acquisition and operational efficiency.

16. Automation Features

Automation reduces costs while increasing productivity.

Check whether the platform automates:

- Lead assignment

- Follow-ups

- Document reminders

- Bureau pulls

- Credit decisions

- Approval routing

- Sanction letters

- Disbursement triggers

Higher automation means lower manual effort.

17. User Experience

Complicated software slows adoption.

Evaluate:

- Dashboard simplicity

- Navigation

- Search capabilities

- Data visibility

- Workflow clarity

- Ease of configuration

An intuitive interface increases team productivity.

18. Implementation Time

Some enterprise LOS projects take months.

Prefer platforms that offer:

- Quick deployment

- Pre-built integrations

- No-code configuration

- Minimal IT dependency

- Cloud hosting

Faster implementation means quicker ROI.

19. Customer Support

Software quality includes vendor support.

Assess:

- Technical assistance

- Training

- Documentation

- Dedicated account managers

- SLA commitments

- Onboarding support

Reliable support minimizes downtime.

20. Future AI Readiness

The future of lending is intelligent automation.

Choose software prepared for:

- Machine learning

- AI underwriting

- Predictive scoring

- Fraud analytics

- Alternate data

- Automated decision engines

Future-ready technology ensures long-term competitiveness.

Questions to Ask Vendors Before Buying

- Can the platform be customized without coding?

- Does it integrate with credit bureaus?

- Is OCR available for document processing?

- Does it support AI underwriting?

- What security certifications are available?

- Can multiple loan products be managed?

- Is mobile onboarding supported?

- What is the implementation timeline?

- Does it support API integrations?

- How scalable is the infrastructure?

Selecting the right Loan Origination Software is a strategic business decision that affects customer experience, operational efficiency, compliance, and long-term growth.

Instead of focusing only on pricing, lenders should evaluate automation capabilities, AI readiness, security, workflow flexibility, integrations, scalability, and reporting features.

By following this checklist, banks, NBFCs, fintech companies, and digital lenders can confidently choose a platform that accelerates lending operations while reducing costs and improving decision-making.

A future-ready Loan Origination System is not just software—it is the foundation of modern digital lending.

FAQ (FAQPage Schema Content)

Q1. What is Loan Origination Software?

Loan Origination Software (LOS) is a digital platform that automates loan applications, borrower onboarding, KYC, underwriting, approval workflows, and disbursement.

Q2. Why is a Loan Origination System important for lenders?

It reduces manual work, speeds up approvals, improves compliance, minimizes errors, and enhances the borrower experience.

Q3. What features should I look for before buying an LOS?

Key features include digital onboarding, automated KYC, business rule engine, AI underwriting, API integrations, document management, analytics, security, and scalability.

Q4. Can Loan Origination Software integrate with credit bureaus?

Yes. Modern LOS platforms typically integrate with bureaus such as CIBIL, Experian, Equifax, and CRIF for automated credit assessment.

Q5. Is cloud-based Loan Origination Software better than on-premise solutions?

Cloud-based solutions generally offer faster deployment, easier scalability, lower infrastructure costs, and remote accessibility.