India’s digital lending ecosystem has witnessed massive growth over the last few years. With the rise of fintech platforms, embedded finance, instant personal loans, BNPL products, MSME lending apps, and API-driven loan processing systems, the Reserve Bank of India (RBI) has significantly tightened regulations to ensure transparency, consumer protection, and responsible lending practices.

The introduction of the Reserve Bank of India (Digital Lending) Directions, 2025 marks one of the biggest regulatory reforms for banks, NBFCs, fintech companies, and Lending Service Providers (LSPs). These directions consolidate previous circulars and strengthen operational, compliance, and borrower protection frameworks across the digital lending ecosystem.

For NBFCs, compliance is no longer optional. Any regulated entity offering digital lending products must ensure that its technology systems, lending operations, data management practices, and customer servicing processes align with RBI guidelines.

At Roopya, we help NBFCs, banks, and fintech companies build RBI-compliant digital lending ecosystems through advanced Loan Origination Systems (LOS), Loan Management Systems (LMS), collections automation, underwriting workflows, KYC integrations, and borrower lifecycle management platforms.

This detailed guide explains everything NBFCs must know about RBI Digital Lending Directions 2025 along with a complete compliance checklist.

What Are RBI Digital Lending Directions 2025?

The RBI Digital Lending Directions 2025 are consolidated regulatory directions issued by the Reserve Bank of India to regulate digital lending activities conducted by banks, NBFCs, and their technology partners. These directions replaced earlier digital lending guidelines issued in 2022 and DLG regulations issued in 2023.

The primary objectives include:

- Protecting borrowers from unfair lending practices

- Ensuring transparency in loan pricing

- Preventing misuse of customer data

- Regulating digital lending apps

- Monitoring Lending Service Providers (LSPs)

- Standardizing disclosures and KFS

- Strengthening cybersecurity and consent architecture

- Ensuring ethical recovery practices

The directions apply to:

- NBFCs

- Banks

- Housing Finance Companies

- Co-operative Banks

- All India Financial Institutions

- Fintech companies working as LSPs

Why RBI Introduced These Directions

The RBI observed several issues in India’s fast-growing digital lending sector, including:

- Hidden charges and misleading APR disclosures

- Unauthorized access to mobile data

- Harassment during loan recovery

- Unregulated lending apps

- Third-party misuse of borrower information

- Excessive dependence on fintech intermediaries

- Lack of transparency in co-lending and multi-lender arrangements

To address these challenges, RBI introduced a borrower-centric framework focusing on accountability, transparency, and responsible digital credit delivery.

Applicability of RBI Digital Lending Directions

The RBI guidelines apply whenever lending is conducted through digital channels such as:

- Mobile lending apps

- Web-based lending portals

- Embedded finance APIs

- Merchant financing platforms

- BNPL systems

- Co-lending platforms

- Digital personal loan applications

- MSME lending portals

If an NBFC uses any fintech company or third-party platform for customer acquisition, underwriting, servicing, collections, KYC, or recovery, the NBFC remains fully responsible for compliance.

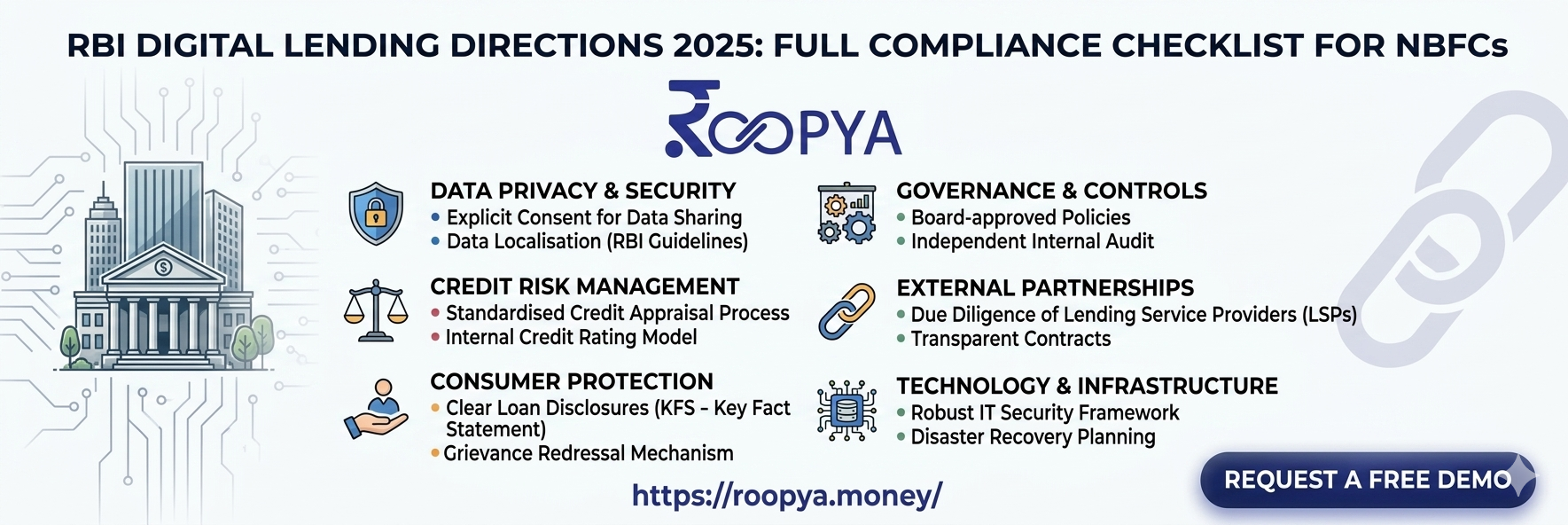

Complete RBI Digital Lending Compliance Checklist for NBFCs

1. Key Fact Statement (KFS) Compliance

One of the most critical requirements under RBI Digital Lending Directions 2025 is mandatory issuance of a Key Fact Statement before loan execution.

The KFS must clearly disclose:

- Annual Percentage Rate (APR)

- Interest rate

- Processing fees

- Penal charges

- Loan tenure

- EMI schedule

- Recovery mechanism

- Cooling-off period

- Grievance officer details

- Total repayment amount

NBFCs must ensure:

- KFS is digitally signed

- KFS is time stamped

- Customer consent is captured

- No hidden charges exist outside KFS

Failure to disclose accurate APR or fees can result in regulatory scrutiny.

2. Direct Loan Disbursal and Repayment

RBI mandates that all loan disbursals and repayments must happen directly between:

- Borrower’s bank account

- Regulated Entity’s bank account

No pass-through or pool accounts operated by fintechs or third parties are permitted.

NBFCs must ensure:

- Direct fund flow architecture

- Account validation systems

- UPI and bank integrations

- Proper reconciliation mechanisms

- Audit trails for every transaction

Modern LOS and LMS platforms should support automated compliance-ready fund tracking.

3. Lending Service Provider (LSP) Due Diligence

NBFCs remain fully accountable for activities performed by LSPs. RBI requires strong due diligence and governance mechanisms for fintech partnerships.

Compliance requirements include:

- Formal outsourcing agreements

- Data protection obligations

- Audit rights

- Customer grievance escalation

- Defined service responsibilities

- Cybersecurity obligations

NBFCs should maintain:

- Vendor risk assessment reports

- LSP monitoring dashboards

- Regular compliance audits

- SLA documentation

4. Digital Lending App (DLA) Registration

RBI now requires reporting of Digital Lending Apps and Platforms through the CIMS portal.

NBFCs must ensure:

- Every DLA is reported to RBI

- Apps display lender information clearly

- Borrowers can identify the regulated entity

- Apps comply with privacy norms

- Unauthorized apps are not used

DLAs must prominently disclose:

- NBFC name

- Interest rates

- Fees

- Customer support information

- Privacy policies

5. Data Privacy and Consent Management

Data protection is one of the strongest pillars of RBI Digital Lending Directions 2025.

NBFCs and fintechs must obtain:

- Explicit borrower consent

- Purpose-specific permissions

- Revocable permissions

The following practices are prohibited unless legally required:

- Accessing contacts unnecessarily

- Accessing photos or media files

- Accessing biometric data without authorization

NBFCs must implement:

- Consent management systems

- Encryption standards

- Role-based access control

- Data retention policies

- Audit logging

6. Data Localization Requirements

All borrower data must be stored within India.

Compliance checklist includes:

- Indian cloud hosting

- Secure backup infrastructure

- Disaster recovery systems

- Data residency policies

- Cybersecurity audits

NBFCs using SaaS-based lending platforms should verify hosting infrastructure and cloud compliance.

7. Cooling-Off Period Compliance

Borrowers must receive a cooling-off or look-up period during which they can exit the loan by paying principal and proportionate charges.

NBFCs should:

- Define cooling-off policy clearly

- Mention it in KFS

- Automate reversal calculations

- Enable digital cancellation requests

This improves borrower trust and reduces disputes.

8. Creditworthiness Assessment

RBI has emphasized responsible lending practices. NBFCs must assess borrower repayment capability before sanctioning loans.

Compliance requirements include:

- Income verification

- Bureau checks

- Fraud checks

- Alternate data validation

- Risk scoring

- Debt-to-income analysis

AI-driven underwriting systems should remain explainable and auditable.

9. Recovery and Collection Compliance

RBI has imposed strict controls on recovery practices.

NBFCs must ensure:

- Ethical collections

- No harassment

- No unauthorized communication

- Proper borrower communication logs

- Trained collection agents

Collections systems should support:

- Automated reminders

- Digital payment links

- Audit-ready communication history

- Recovery agent tracking

10. Grievance Redressal Mechanism

Every regulated entity must establish a borrower grievance redressal mechanism.

Requirements include:

- Dedicated grievance officer

- Contact details in app and KFS

- Escalation matrix

- Complaint tracking

- Resolution timelines

NBFCs should deploy omnichannel support systems including:

- Chatbot

- IVR

- Ticketing systems

- WhatsApp support

11. Reporting to Credit Information Companies (CICs)

All digital loans must be reported to Credit Information Companies irrespective of loan size or tenure.

NBFCs should ensure:

- Accurate bureau reporting

- Timely updates

- Structured data formats

- Dispute resolution workflows

Failure in bureau reporting may impact regulatory standing.

12. FLDG and DLG Compliance

RBI has formalized Default Loss Guarantee (DLG) rules for fintech partnerships.

Key requirements include:

- Defined DLG structure

- DLG cap limits

- Eligible guarantee providers

- Board-approved policies

- Proper accounting treatment

NBFCs must avoid unregulated credit guarantees outside RBI norms.

13. Multi-Lender Arrangement Compliance

If a platform aggregates multiple lenders, borrowers must receive complete transparency about:

- Lender identity

- Ranking logic

- Loan offers

- Pricing differences

NBFCs should implement:

- Transparent offer display

- Consent-based lender selection

- Audit-ready recommendation engines

14. Technology and Cybersecurity Standards

Digital lenders must maintain strong cybersecurity controls.

Compliance checklist:

- VAPT testing

- API security

- Encryption

- SIEM monitoring

- Access management

- Incident response plans

- SOC monitoring

Technology systems must support RBI audit readiness.

15. Audit and Compliance Monitoring

NBFCs should conduct regular audits for:

- Lending operations

- Data access

- Consent logs

- Recovery activities

- LSP operations

- Cybersecurity posture

Compliance dashboards should provide:

- Real-time monitoring

- Exception reporting

- Audit trail generation

- Automated alerts

Technology Challenges Faced by NBFCs

Many NBFCs struggle with:

- Legacy systems

- Manual compliance tracking

- Multiple vendor integrations

- Poor data governance

- Fragmented LOS/LMS architecture

This is where advanced fintech infrastructure becomes critical.

How Roopya Helps NBFCs Achieve RBI Compliance

Roopya provides enterprise-grade digital lending infrastructure for NBFCs, fintechs, and banks.

Key capabilities include:

- RBI-compliant Loan Origination System

- Automated KFS generation

- Digital onboarding and eKYC

- Consent management systems

- Bureau integrations

- Loan Management System

- Collections automation

- API-based lending workflows

- Audit-ready reporting

- Multi-lender orchestration

- Secure cloud infrastructure

- DLA-ready borrower journeys

Roopya enables lenders to launch compliant digital lending products faster while reducing operational risks.

Benefits of RBI-Compliant Digital Lending Infrastructure

NBFCs adopting compliant lending technology gain:

Faster Loan Processing

Automation reduces TAT and improves borrower experience.

Reduced Regulatory Risk

Compliance-ready systems minimize RBI scrutiny.

Better Borrower Trust

Transparent loan disclosures improve customer confidence.

Improved Portfolio Quality

Advanced underwriting reduces default risk.

Scalable Operations

Cloud-native platforms support high-volume lending.

Stronger Data Security

Secure infrastructure protects customer data.

Future of Digital Lending in India

India’s digital lending market is expected to grow rapidly across:

- MSME lending

- Consumer finance

- Embedded lending

- Supply chain finance

- Co-lending

- Agri-finance

- Neo-banking ecosystems

However, growth will increasingly depend on regulatory compliance, transparency, and secure technology architecture.

NBFCs that invest in RBI-compliant lending infrastructure today will be better positioned for sustainable long-term growth.

Final Thoughts

The RBI Digital Lending Directions 2025 represent a major transformation in India’s digital credit ecosystem. The focus has shifted from aggressive growth to responsible, transparent, and borrower-centric lending.

For NBFCs, compliance is now deeply connected with technology architecture, operational workflows, data governance, and customer experience.

Modern lending organizations need integrated LOS, LMS, compliance automation, cybersecurity controls, and borrower protection mechanisms to remain competitive and regulator-ready.

Roopya helps NBFCs, fintechs, and banks build scalable and RBI-compliant digital lending ecosystems with advanced automation, workflow management, underwriting systems, and borrower lifecycle platforms.

As regulatory oversight increases, compliant digital infrastructure will become the foundation of successful lending businesses in India.

FAQ

What are RBI Digital Lending Directions 2025?

The RBI Digital Lending Directions 2025 are consolidated regulations issued by RBI to govern digital lending operations conducted by banks, NBFCs, and fintech companies.

Who must comply with RBI Digital Lending Guidelines?

Banks, NBFCs, Housing Finance Companies, fintechs acting as Lending Service Providers (LSPs), and digital lending platforms must comply.

What is a Key Fact Statement (KFS)?

A Key Fact Statement is a mandatory borrower disclosure document containing APR, fees, repayment schedule, loan tenure, and grievance information.

Are fintech companies directly regulated under RBI Digital Lending Directions?

Fintech companies working as LSPs are indirectly governed through regulated entities such as NBFCs and banks.

What is FLDG in digital lending?

FLDG stands for First Loss Default Guarantee or Default Loss Guarantee, which governs risk-sharing arrangements between fintechs and regulated entities.

Can NBFCs use third-party lending apps?

Yes, but NBFCs remain fully responsible for ensuring compliance by those apps and platforms.

Is customer consent mandatory in digital lending?

Yes. Explicit and purpose-specific borrower consent is mandatory for data collection and usage.

What data access is restricted under RBI guidelines?

Apps cannot access contacts, photos, media, or biometric data without explicit lawful requirements and borrower consent.

Why is direct disbursal important?

RBI mandates direct loan disbursal between the regulated entity and borrower to prevent misuse of intermediary accounts.

How can Roopya help NBFCs?

Roopya provides RBI-compliant Loan Origination Systems, Loan Management Systems, collections automation, borrower onboarding, and digital lending infrastructure.