Businesses rely on healthy cash flow to operate efficiently, pay employees, invest in growth, and meet financial obligations. However, maintaining financial stability involves much more than simply generating sales. Two business functions that are often misunderstood are outsourced credit control and loan processing. Although both relate to business finances, they serve very different purposes.

Many business owners mistakenly believe that improving access to loans solves cash flow problems. In reality, better management of customer payments can often reduce the need for borrowing altogether. Understanding the difference between outsourced credit control and loan processing helps businesses choose the right solution for their financial needs.

This guide explains how each service works, their key differences, and when businesses should consider using them.

What Is Outsourced Credit Control?

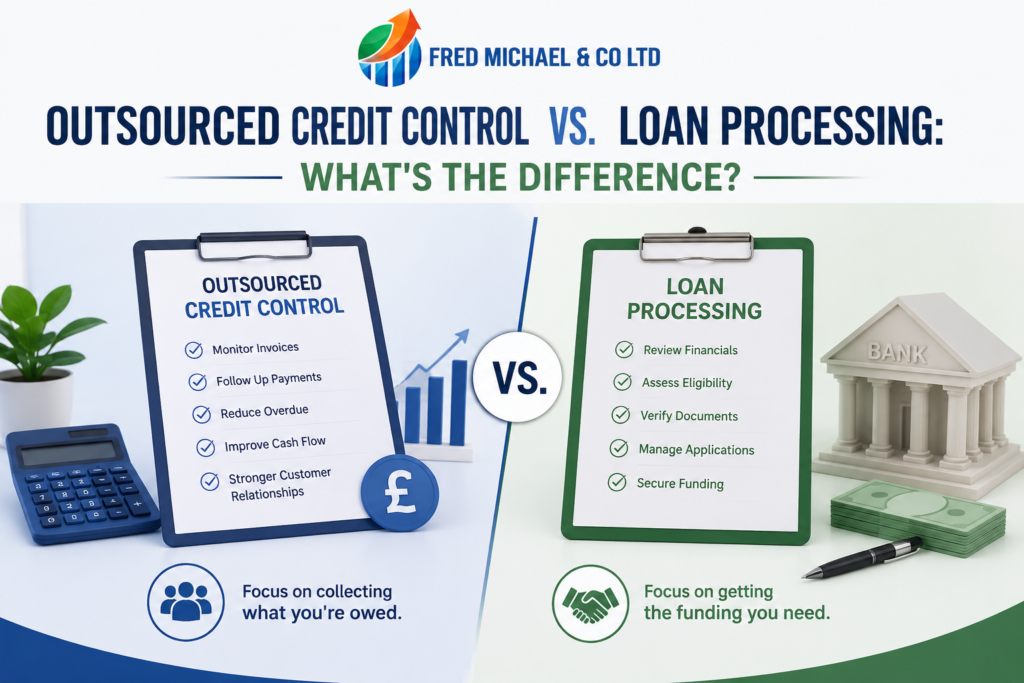

Outsourced credit control is the process of hiring external professionals to manage customer invoices, monitor outstanding payments, and encourage timely payment from clients.

Rather than relying on internal staff, businesses delegate these responsibilities to specialists who use structured processes to improve payment collection while maintaining positive customer relationships.

The main objective is simple: ensure customers pay on time so the business maintains consistent cash flow.

Typical credit control responsibilities include:

- Issuing customer invoices

- Monitoring outstanding balances

- Sending payment reminders

- Following up overdue accounts

- Maintaining customer communication

- Producing debtor reports

- Reducing late payments

- Supporting healthier cash flow

Professional credit control management London enables businesses to improve working capital without increasing debt or relying heavily on external financing.

What Is Loan Processing?

Loan processing is a completely different financial activity.

Instead of collecting money already owed by customers, loan processing focuses on securing external funding from banks or financial institutions.

During loan processing, financial information is gathered, verified, and assessed before a lender decides whether to approve financing.

Loan processing generally includes:

- Collecting financial documents

- Reviewing business income

- Verifying assets and liabilities

- Assessing credit history

- Evaluating repayment ability

- Completing lender documentation

- Preparing applications for approval

The goal is to obtain funding that supports business activities such as expansion, equipment purchases, or working capital requirements.

The Main Difference

The simplest way to understand the difference is this:

Outsourced credit control helps businesses collect money they have already earned.

Loan processing helps businesses borrow money they do not currently have.

While both influence business finances, their objectives are entirely different.

One improves internal cash flow by reducing overdue payments, while the other increases available capital through borrowing.

When Should a Business Use Outsourced Credit Control?

Many growing businesses experience delayed customer payments.

Even companies with strong sales can struggle if invoices remain unpaid for long periods.

Businesses should consider outsourced credit control when they experience:

- Increasing overdue invoices

- Slow customer payments

- Limited internal resources

- Cash flow pressure

- High administrative workload

- Growing customer accounts

Rather than hiring additional employees, outsourcing allows businesses to access experienced professionals who specialise in payment collection.

This often leads to faster payments and improved financial stability.

When Is Loan Processing More Appropriate?

Loan processing becomes useful when businesses need additional funding for specific purposes.

Examples include:

- Opening a new location

- Purchasing equipment

- Expanding production

- Investing in technology

- Hiring additional staff

- Supporting seasonal growth

Loans provide businesses with immediate capital, but they also create repayment obligations and interest costs.

For this reason, borrowing should normally support planned investment rather than covering preventable cash flow shortages.

Benefits of Outsourcing Credit Control

Many businesses underestimate the impact overdue invoices have on profitability.

Professional credit control offers several advantages.

Improved Cash Flow

Consistent payment collection improves liquidity and ensures businesses have sufficient funds available for daily operations.

Reduced Administrative Work

Business owners and finance teams spend less time chasing unpaid invoices, allowing greater focus on strategic activities.

Better Customer Communication

Experienced credit controllers use professional communication methods that encourage payment while maintaining strong customer relationships.

Lower Risk of Bad Debt

Early follow-up reduces the likelihood that overdue accounts become uncollectable.

Greater Financial Visibility

Regular reporting helps businesses understand payment trends and identify customers who consistently pay late.

Benefits of Loan Processing

Loan processing also provides important advantages when funding is genuinely required.

Access to Capital

Businesses can obtain funding for expansion projects or significant investments.

Supports Business Growth

Loans can provide resources needed to enter new markets or purchase valuable assets.

Preserves Cash Reserves

Borrowing allows businesses to maintain operational cash while funding large investments separately.

Structured Repayment

Most business loans offer predictable repayment schedules that support long-term financial planning.

Can Businesses Benefit from Both?

Yes.

Many successful businesses use both services at different stages.

For example, a company may improve payment collection through outsourced credit control while also applying for finance to expand operations.

The two services are complementary rather than competitive.

Healthy cash flow also strengthens loan applications because lenders prefer businesses with reliable financial management.

The Importance of Accurate Financial Records

Whether improving payment collection or applying for finance, accurate financial information is essential.

Reliable accounting and bookkeeping services ensure financial records remain organised, making it easier to monitor business performance, prepare financial reports, and provide supporting documentation when required.

Accurate records improve decision-making and create greater confidence for both lenders and business owners.

Strategic Financial Guidance Matters

Financial decisions should always support long-term business objectives rather than simply solving short-term problems.

Working alongside a knowledgeable small business financial advisor London allows business owners to evaluate whether improving collections, reducing expenses, restructuring finances, or seeking funding represents the most suitable solution.

Professional financial advice helps businesses make informed decisions rather than reacting to immediate financial pressures.

Planning for Sustainable Growth

As businesses expand, financial management becomes increasingly complex.

Some organisations benefit from experienced financial director services that provide strategic oversight, budgeting support, financial forecasting, risk management, and long-term planning without employing a full-time finance director.

This level of expertise helps businesses prepare for growth while maintaining financial discipline.

Choosing the Right Solution

Every business experiences different financial challenges.

If delayed customer payments are creating cash flow problems, improving credit control may deliver immediate benefits without increasing debt.

If expansion requires additional investment beyond existing cash reserves, loan processing may provide the funding needed to achieve business objectives.

The best solution depends on understanding the underlying financial issue rather than treating every cash flow concern as a borrowing problem.

Businesses such as Fred Michael & Co Ltd recognise that effective financial management involves balancing strong payment processes, accurate financial reporting, and strategic planning to support long-term business success.

Final Thoughts

Outsourced credit control and loan processing are often discussed together because both relate to business finances, but they perform very different roles.

Credit control focuses on collecting outstanding customer payments, strengthening cash flow, and reducing financial pressure. Loan processing focuses on securing external funding for investment and business expansion.

Understanding these differences enables business owners to make more informed financial decisions and choose solutions that support sustainable growth. By evaluating cash flow, reviewing business goals, and maintaining accurate financial records, businesses can build stronger financial foundations while reducing unnecessary financial risk.

Frequently Asked Questions (FAQs)

1. What is outsourced credit control?

Outsourced credit control involves hiring specialists to manage customer invoices, monitor overdue payments, and improve cash flow through professional payment collection.

2. What is loan processing?

Loan processing is the process of preparing, verifying, and submitting financial information to lenders when applying for business finance.

3. Which service improves cash flow faster?

If delayed customer payments are the main issue, outsourced credit control often improves cash flow more quickly because it focuses on collecting existing outstanding invoices.

4. Can a business use both services?

Yes. Many businesses improve payment collection through credit control while also using loans to finance expansion or major investments.

5. How do accurate financial records support both services?

Accurate records help businesses monitor cash flow, manage customer accounts, prepare loan applications, demonstrate financial stability, and make informed business decisions.